Changes in rules on old HDB leasehold flats and how it affects young couples

In May 2019, the government relaxed rules for older citizens looking to buy old HDB leasehold flats using more money from their CPF accounts. This was in response to the older HDB flat losing value due to the 99 years leasehold and how the original CPF rules make it difficult for older couples to buy them.

The details of the changes can be read here (More Flexibility to Buy a Home for Life While Safeguarding Retirement Adequacy).

While the focus of the changes are very healthy from the point of view of a mature couple and the many good examples are given to illustrate so, it is also important to look at the changes and understand its significant impact on younger couples.

More importantly, it is good to approach it from the real on-the-ground impact of the rules rather than just some nice infographics provided to support the case.

What are the changes to the CPF rules for old HDB leasehold properties

Firstly, the total amount of CPF that can be used for property purchase will depend on the extent the remaining lease of the property can cover the youngest buyer to the age of 95. This “total amount of CPF that can be used” is known as the Valuation Limit (VL). For old HDB leasehold flats with about 60 years of remaining lease, the youngest owner just needs to be 35 years and above, and the whole 100% purchase can be covered by CPF up to the valuation limit.

Secondly, CPF members will now need to have a property with sufficient remaining lease to cover them until at least the age of 95, before they can withdraw their CPF savings above the Basic Retirement Sum. That means, at the time of CPF withdrawal (55 years old as at 2019), they should have a property that has at least a leasehold of 40 years (to cover them up to 95 years).

Before they can even withdraw a single cent….. (cue… “Return my CPF” slogans)…. 🙂

The press release stated that “this change is not expected to affect most CPF members, as all HDB flats and the vast majority of private properties have leases that can last a 55-year old member until the age of 95. “. That is true for now. That might not be true in 15-20 years time when more and more old HDB leasehold flats reaches the 60 years mark (leaving them with a remaining lease of 39 years).

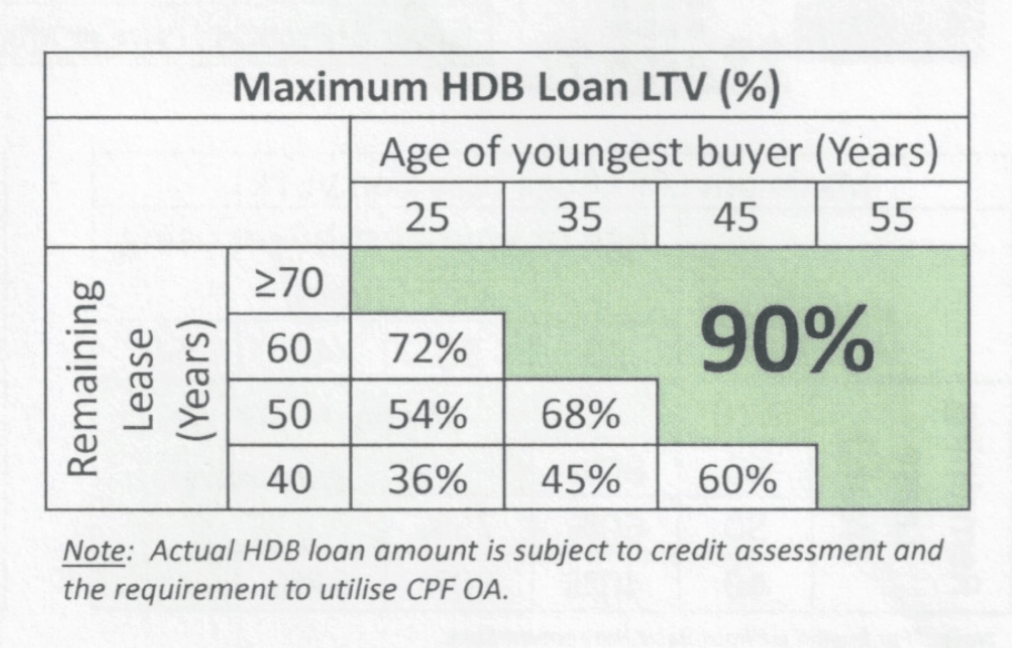

Lastly, buyers will now only be able to take an HDB housing loan of up to the full 90% Loan-to-Value (LTV) limit, if and only if the remaining lease of the flat can cover the youngest buyer to the age of 95. So, again, to get the full HDB loan, the youngest owner need to be 35 years old if they are buying a property with 60 years lease left.

Let’s be clear here. The changes are very good and positive for an older couple looking to buy a old HDB leasehold home (especially if it is to downgrade from a bigger flat to a smaller flat in an older estate which they are familiar with and the children has grown up etc).

The rules changes will allow the older couple to buy a old HDB leasehold flat with full CPF usage (and not so importantly, the use of a full LTV loan). At their age, after selling the large flat, it will be great to be able to immediately use ALL their CPF proceeds to pay for the smaller old HDB leasehold home without any limitation and without any cash top up and loans.

This is because, for the first time, an older couple can now use the CPF up to the full valuation limit to purchase a old HDB leasehold flat.

Of course, It was very prudent for the authorities to also ensure that a young couple to be able to buy a home that last them till 95 years old. So the advice was given clear and loud. It is probably better for them to avoid an old HDB leasehold flat and instead opt for a newer BTO flat.

On paper, all seemed good. But in reality, there are some immediate impact which a competent and knowledgeable real estate agent should point out the younger couple.

This is especially so since most younger buyers are purchasing the HDB flat on a Do It Yourself (DIY) basis and might not have all the information.

“A little knowledge is a dangerous thing”

Alexander Pope (1688 – 1744)

How does these changes for older HDB leasehold flats affect younger couples

I want to bring a more realistic approach to the changes from the ground. This is from my work as a housing agent and it is interesting to see how this actually affects younger couples who were interested to buy an old HDB leasehold property.

The key principle in the changes is this statement : “if the remaining lease of the flat can cover the youngest buyer to the age of 95“.

Simply put, the sum of (the age of the youngest buyer of the older HDB leasehold flat + the remaining lease for this older HDB leasehold flat) must be equal or more ( >= ) than 95 years old.

So a very young couple and a very old HDB leasehold flat is a very bad combination.

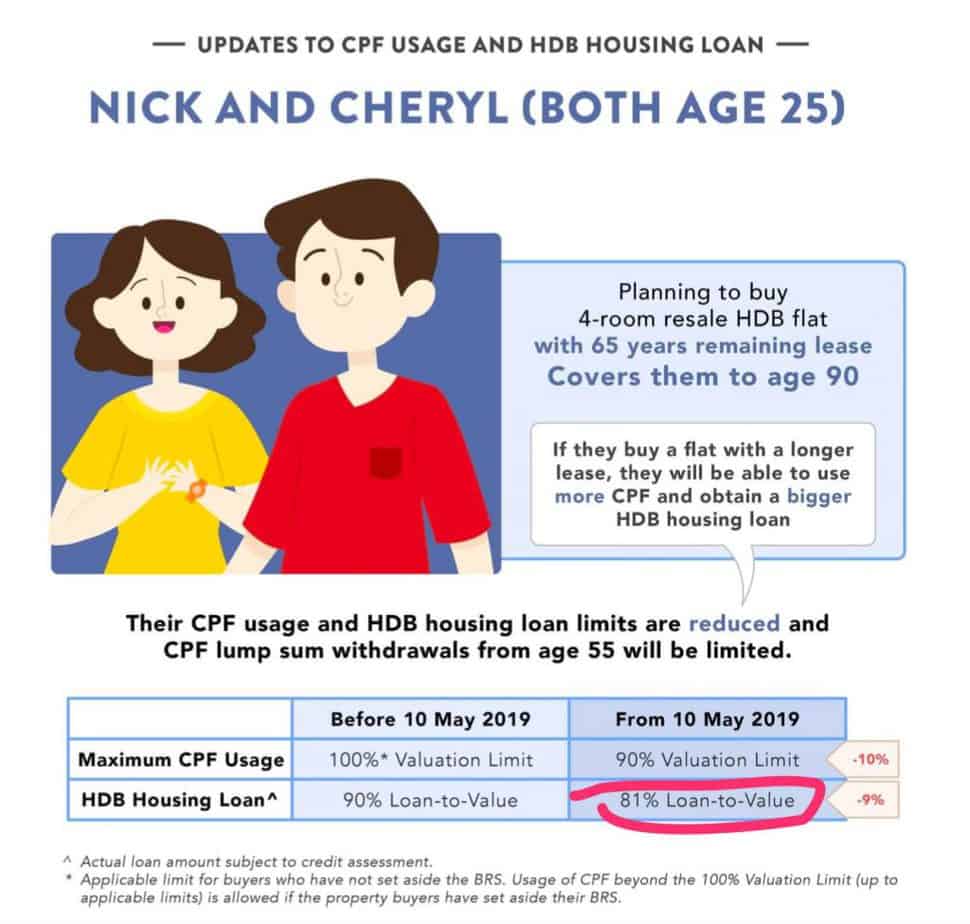

In the press release, after a couple of examples of very happy older couples, it finally did give one example of Nick and Cheryl (both who are 25 years old and looking to buy a HDB flat with 65 years remaining lease) and how they now “suffer” prudently 😉

While many may just focus on the reduction of Valuation Limit (VL) and might even wonder what it meant, the reduction of a HDB Housing Loan from 90% LTV to 81% LTV (the red circled part) is actually a more significant issue on the ground.

This is because the first “payment” for the HDB flat is the downpayment (and not something called Valuation Limit).

And behold, for the young couple buying the old HDB leasehold flat, the downpayment has just went up. Now. Right now.

To be fair, there is a chart given. Read it. Understand it. Ignore it at your own peril.

A young couple (a man 28 years old and a young wife of 25 years old) who wanted to buy a old HDB leasehold flat with remaining lease of 50 years will now….. have to…. pay 46% downpayment as the loan is now only 54%.

When we as housing agents work with younger couples, we need to make sure they are aware that there is a change in the LTV and what it means for their pockets. Immediately.

Which scenario is really true on the ground

Unfortunately for a small group of young couples, this has some significant impact.

This will usually happen when the couple is around 30 years old (good time to get married, have kids and help Singapore’s population growth 🙂 ) AND when they want to live near their parents in older estate (which is necessary to help them in taking care of their babies) AND the older estates are mature estates (which are usually higher in resale prices).

An example of the impact on a young couple

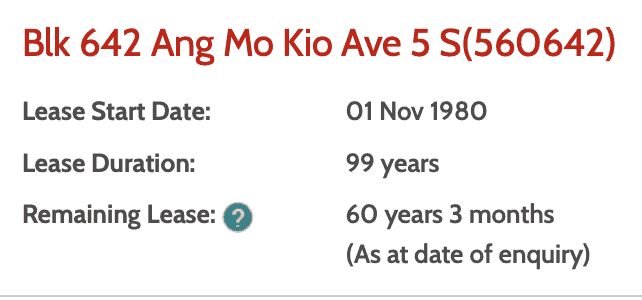

Let’s look at a case I met recently. The couple are both 28 years old (both the boy and the girl) and they are interested in this HDB five room flat along Ang Mo Kio Avenue 3 which has a remaining lease of 60 years.

You can find out the remaining lease of a HDB flat using this link to HDB Map Services.

As an example, as at today, Blk 642 in Ang Mo Kio has a remaining leasehold of 60 years.

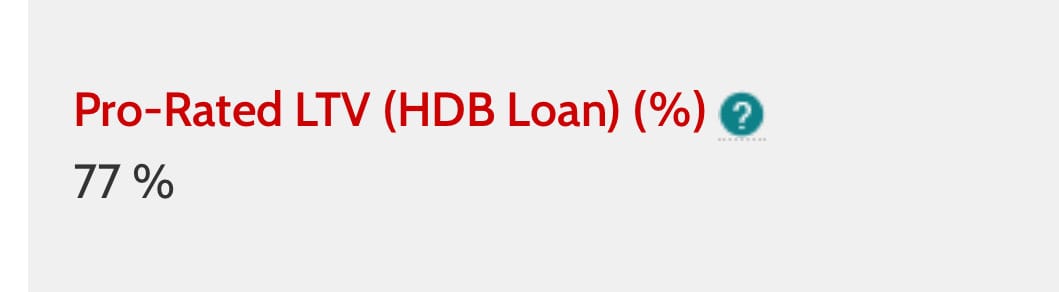

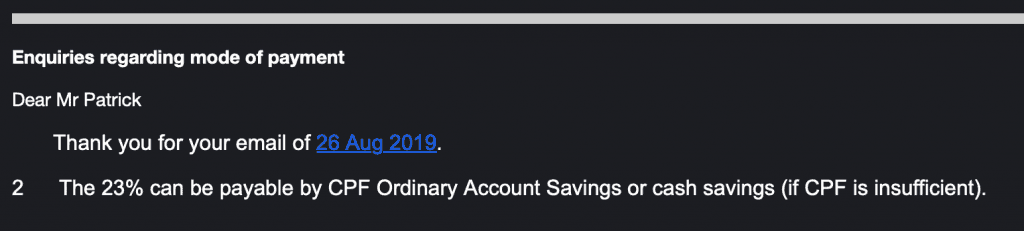

Let’s go to HDB web site and do a financial plan at “Enquiry on Resale Financial Plan” page.

If you input the information as per above (Age of Youngest and Leasehold Remaining), HDB will now tell you that your LTV (Loan to Value) of HLE loan has been pro-rated to 77%.

What does 77% mean for the young couple ? This simply means that the Loan to Value (LTV) has been reduced to 77%. That means they must now pay an increased downpayment of 23% of the value of the property and then they will be able to get a reduced loan of 77% of the value of the property.

Previously, it is possible to have a 90% LTV for HDB HLE Loans (borrowing from HDB and not private banks). The young couple can just pay 10% downpayment and have a 90% loan from HDB.

Now that LTV has been reduced to 77%, the loan amount has dropped and hence the immediate first downpayment has gone up.

And when this happens in mature estate where the property prices are higher than other non mature estates, it has significant financial impact.

Going back to the example above, let’s work out the numbers now

The HDB flat could be selling for $600,000 (that is a reasonable price for a 5 room HDB flat in Ang Mo Kio).

That mans the young couple must have 23% in downpayment (=23% of $600,000 = $138,000) while the HDB HLE Loan is now 77% (=77% of $600,000 = $462,000).

How many young couples have $138,000 in their CPF ordinary account at the age of 28 years old ?

Can we use all our CPF for the increase in downpayment due to the pro-rated LTV

All is not lost ! Do not despair if you are a young couple in the above scenario.

I reached out to HDB and confirmed that the whole 23% downpayment for the HLE Loan can be paid by CPF. Of course if the CPF is not enough, then you need to top up with cash.

What about private bank loans ? In the case above, there is no change. For Private HDB bank loans, the downpayment is already 25% (consisting of 5% cash and 20% CPF) which is already more than the 23% calculated above. So it is not an issue. Private bank loans are very prudent long ago 🙂

HDB CPF Grants to the rescue

Young couples do not really have a lot in their CPF ordinary account to pay for the increased downpayment. This is just a nature of their age and the length of time they started working and the amount of salary they have at that age. You cannot beat physics.

It will not be surprising then if they don’t have enough CPF to pay for the above increased downpayment and need to top up the difference in cash.

Or maybe not.

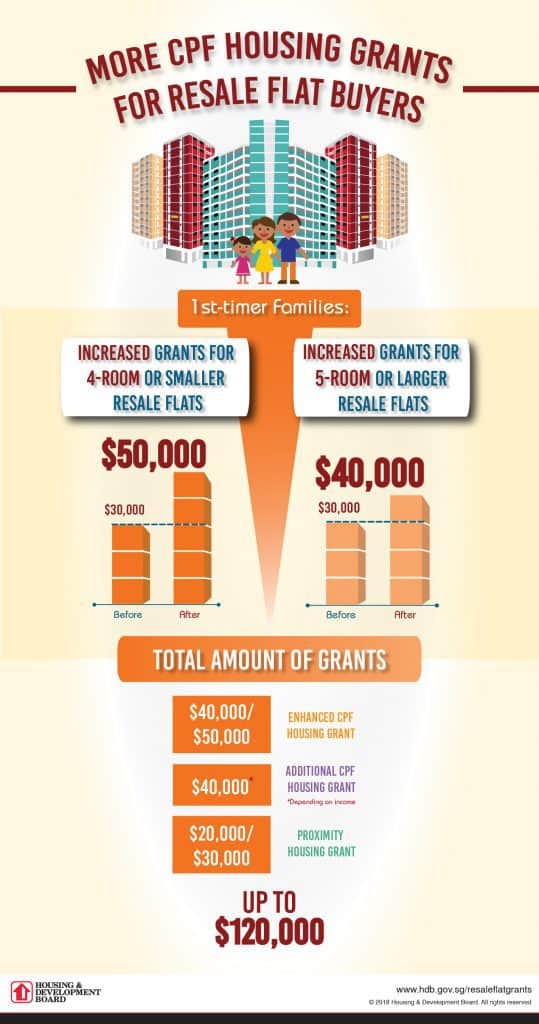

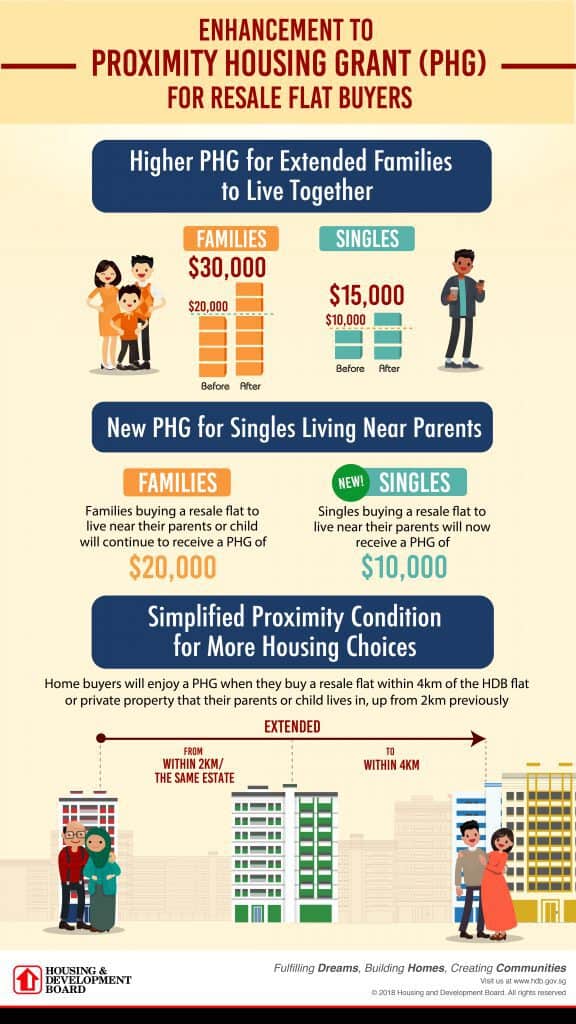

The Government does provide a large amount of HDB grants to first time house owners. For example, there are housing grants such as enhanced CPF housing grant and additional housing grant (AHG).

More significantly, for our example, the younger couple who wanted to purchase an older flat to stay within 4 km of the parents, the government also provides a very good Proximity Housing Grant (PHG).

This can give the younger couple of up to $30,000 ($20,000 for staying near, $30,000 for staying together… you can decide if $10,000 is worth the nagging of your mother in law.. kidding 🙂 ).

Looking at the amount of grants, the young couple could have up to maybe $100,000 help from the government. Which will more than cover the $138,000 needed in our example.

And more help is coming in September 2019 too

Also in September 2019, the government will be announcing more help for first-timers buying new and resale flats so you can expect that the above example will be further resolved.

Hence, all might still be good !!

What about the commonly talked about impact on VL

There is, of course, the impact of the valuation limit (VL) too. You can use the CPF Housing Withdrawal Limits Calculator to see what is the impact on the amount of CPF the young couple can use for their flat. According to the example of Nick and Sheryl, it has dropped from 100% to 90%.

What does it mean on the ground ? Honestly for housing agents, we don’t really care about VL (Valuation Limit). And buyers don’t really ask or know or care about.

It is a concept more far out into the future. It is about when your allowed CPF usage (known as valuation limit for HDB flats) run out and you must use cash to pay for the monthly instalments. And it WILL run out at some point (as the original downpayment from CPF and monthly instalments you are paying by CPF exceeds this limit eventually).

But when we sell a flat or buy a flat, this is not really something both the buyers, the sellers and the housing agents will typically discuss or even think about. It is not that VL is not important. It is ! It is just that at the time of purchase, people don’t typically think or worry about it.

Which is hence, important to see how in reality, the real impact on the ground is not the same impact that the authorities were stressing.

Not the valuation limit. But the Loan to Value limit.

If you are buying old resale flats (whether young or old), do take note of the 5 important checks before buying.

Patko

Patko

Member discussion